No, I’m not referring to the bizarre incident where a customer tried to return this plastic corn after her grandson cooked it, thinking it was real. A few weeks ago I wrote about my run-in with the Asset Protection team at Walmart. One of the Asset Protection Associates had seen me buying money orders at another Walmart and assumed I was up to something.

He alerted his colleague, rushed in, and accused me of making multiple trips to the same store in order to avoid filling out the FinCen form. That’s obviously not true, since I only make one visit per day and always fill out the form.

The associate told me he’d research the store’s policy about splitting a $10,000 purchase across five transactions. At first, he thought it was ok as long as it was during one visit and I filled out the paperwork. Then he seemed unsure. So he told me to come back the following Saturday and he’d notify the entire staff about it.

I wasn’t able to return that weekend. When I stopped by the store later, my regular cashier spotted me in line and said the money order machine was broken. I finally went back to the store on Tuesday and saw the same cashier who was there during the incident, along with the store manager.

The manager is a really nice guy and has always been ok with my money order purchases. I was relived when he didn’t object to a $10,000 purchase split across 5 transactions.

When I was done with money orders, I asked if I could pay bills and use more than one payment form. In the past, none of the cashiers were able to figure that out. In fact, the last time I tried, the cashier couldn’t even find Discover in their system.

He proceeded to process my bill payment. He also pointed out that there are some shady characters who try to commit fraud with these cards but, “We haven’t heard anything bad about you, so I trust you.” I had a few more bills to pay, but decided to see if if was safe to go back to the other store.

I went to the store where I had my initial run-in with the Asset Protection Associate. It’s the same store where the cashier told me I could only buy money orders in a single transaction and only make payments on credit cards that belonged to me.

During my conversation with the Asset Protection Associate, he claimed the first part was not true. As long as I did it all in one visit, I could split my purchases across five transactions. Anyway, the same obnoxious cashier was working and he had the usual attitude problem.

However, to my surprise he didn’t ask for my ID when I asked to pay my Discover bill. This is the same guy who insisted during the previous visit that I present my ID, which had to match my card. Maybe it was his bad mood, but he wasn’t enforcing the rules that day.

I asked if the Asset Protection guy was around. He said he hadn’t seen him in a couple of days. It had been well over a week since my conversation with the Asset Protection guy. Neither store gave me trouble for bill pay or money order purchases. So I assume it has all been worked out.

This is a big relief since I’m trying to ramp up my manufactured spending efforts in the next few months. I will need things to be easier going forward. Thankfully, I’m back in everyone’s good graces and can continue to buy money orders and do Bill Pay as well.

Anyway, I thought I’d provide an update for those folks who wondered how it all turned out.

Always like to hear good news. I’d say this qualifies.

How do you liquidate the money orders? I’m reading up on MS and I’ve only read that banks get weird when you try to deposit many money orders.

They do, which is why I have a separate bank account for mo deposits. That way, if it gets shut down, it won’t affect my normal banking activities.

I am dipping my toe into MS. I ordered a modest gift card from giftcards.com to test the processes out using your Yazing portal link, thanks for being so comprehensive with your blog. And your Calais post was beautiful.

Thank you Austin!

Are u liquidating VGCs? Where are u getting $2000 VGCs?

Not single $2k GC’s.

Ariana is liquidating 4x $500 GC’s per transaction – which is the max. no. Walmart will allow.

I’m using $300 – $500 Visa gift cards from Staples and Giftcards.com.

Becareful of the BP rout. Once you pass a certain level, things get squirrely. Small time players will be fine but when you get into the 150-200k range there is a chance you hit their radar for a shutdown.

I’ve been at probably around $20k tops for bill pay. I highly doubt I’ll get to the $150k range, but I appreciate the heads up.

What other credit card bills you can pay at Walmart?

At my store, the cashiers can’t pull up anything other than Discover. But I know folks who’ve paid Citi and Barclays (and got their Barclays Arrival accounts shut down).

So interesting the variances between states, cities and individual stores. Tried to use Bill pay at Walmart with a debit card. … She looked at me like I was from another planet. Have you ever done bill pay with a debit card and skipped the money order process?

Sorry. Tried to Bill Pay with a MO and she thought I was crazy. Can I skip it and use BP using a debit card?

I do bill pay too, but MO’s are how I liquidate the most gc’s. Depending on the store, I’ll do both in the same visit.

Last weekend the MoneyCenter cashier wouldn’t let me do two transactions for MOs. He whipped out some handbook that said all MOs need to be on the same receipt/transaction. He didn’t care that you can only do $2k in a single transaction/receipt.

I don’t know how you get away with it. At my local supermarket they are always turning me down because they say that it’s a gift card and according to them it’s not allowed.

have you tried Walmart?

I must admit that I have not. I will give it a try today. Thanks

It is worrisome that liquidating at Walmart is getting harder and harder.

Hello, I’ve really enjoyed reading your blog for the last several months. I’m starting to ramp up my MS. I really haven’t been doing much yet. I was curious, how much is too much you think before getting shutdown? I’d like to MS UR and SPG points through giftcards.com and was wondering if $4000 a week per card is too much or if I have room for more. Thanks!

Now that Amex has made it pretty clear that you can’t buy reloadable cards or GCs for bonus offers I wouldn’t be surprised if they shutdown your account and trashed all your points. At least with Chase if they shut you down they give you a month to transfer out your earned points, though you may lose the points from the pending statement period. I used to do SPG but not anymore. And I can’t even remember the last time I MS’d on any Chase product. I have a legit business and I value my Chase relationship.

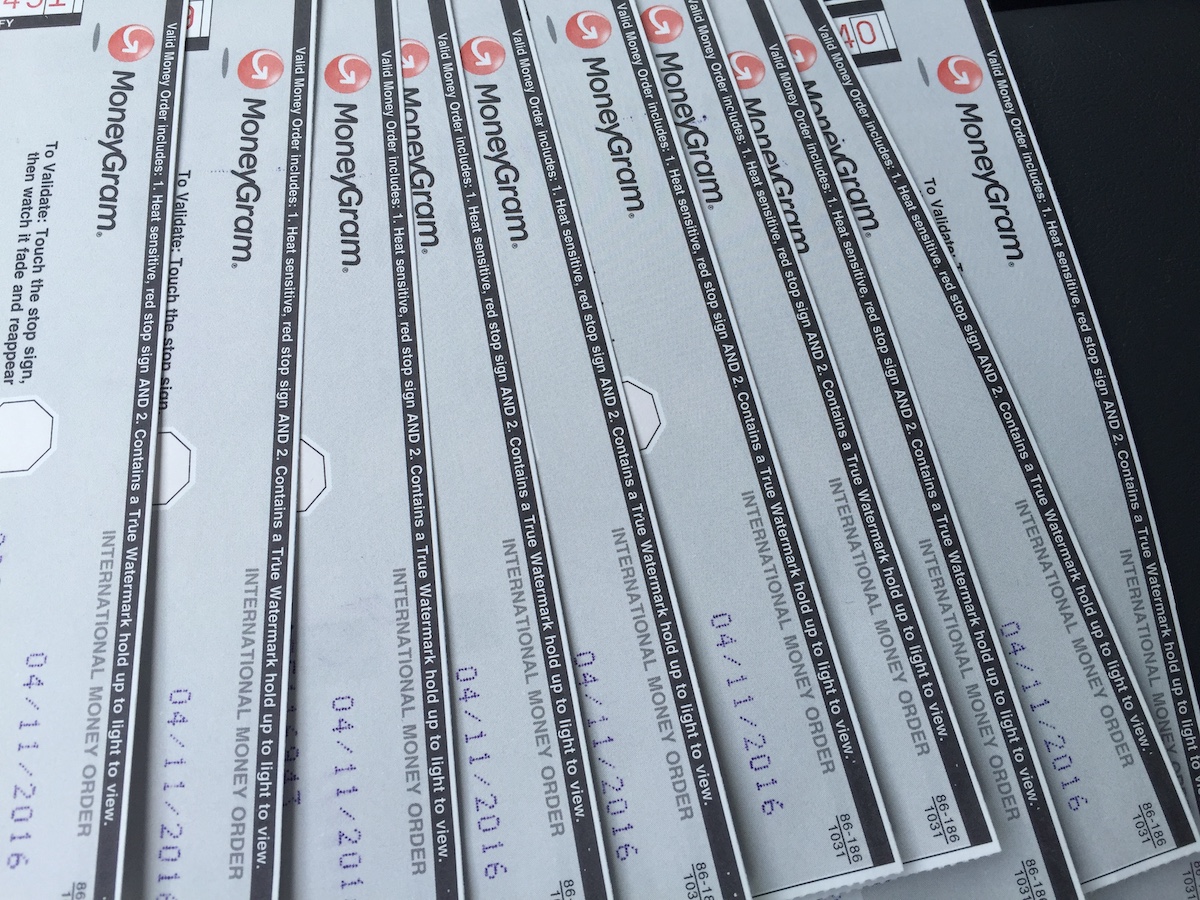

I have a large property tax payment coming up, and I’m thinking of using Walmart MOs purchased with VGCs. I understand I can use a max of four per transaction, but what demonination of MOs are you purchasing? Your beginners guide says Walmart’s max is $1000, but this post has a picture of five MOs and mentions $10K spread over five transactions.

Thanks for all your advice!

The $1k max refers to the fact that each money order cannot be more than $1k. I usually buy $2k per transaction and split payment across four $500 cards, paying the fee in cash.