The new Citi 48-month restriction on AAdvantage credit card sign-up bonuses is going to disappoint many people. Previously, you could get the same sign-up bonus on these cards every 24 months (before that went into effect, it was 18 months). So now, you have to essentially wait four years between sign-up bonuses.

That makes the AAdvantage cards much less churnable, which is unfortunate because the card has always offered a solid sign-up bonus.

If you’re considering applying for a new AAdvantage credit card, here’s everything you need to know about the new Citi 48-month restriction:

What this means for credit card churning

One 50,000 – 75,000 mile sign-up bonus every four years is not great. The new Citi 48-month restriction on AAdvantage credit card sign-up bonuses means you should probably time your applications to get a higher sign-up bonus.

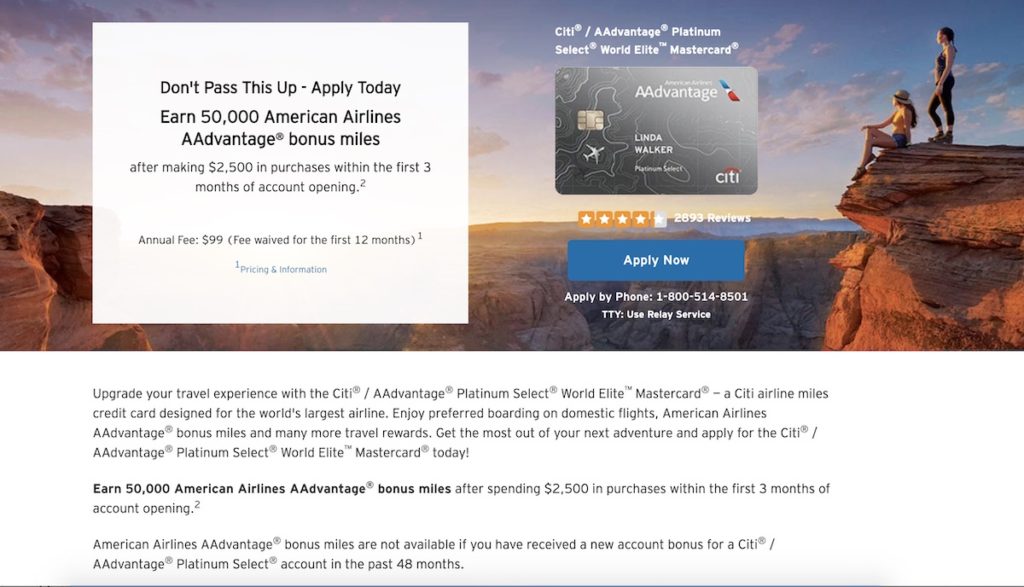

At the moment the Citi AAdvantage Platinum card offers 50,000 miles after $2,500 spent in three months. Often, Citi will run targeted or public promotions for 65,000 and 75,000 bonus miles instead. Now that you can only get this sign-up bonus every four years, you might want to hold out for a bigger bonus.

Keeping the Citi AAdvantage Platinum card long-term?

With the 48-month wait period between sign-up bonuses, you might be wondering if it’s still a good idea to toss the card after the first year. It might not be, if you want to continue earning AAdvantage miles on regular expenses as well as manufactured spending.

I’m not a big credit card churner, so the $125 flight discount is reason enough to keep my AAdvantage card long-term. However, I was also tempted by another ~60,000-mile sign-up bonus. Obviously, that decision has now been made for me: Flight Discount voucher it is.

Why the Citi 48-month restriction isn’t bad

The new Citi 48-month restriction on AAdvantage sign-up bonuses isn’t all bad. That’s because Citi now treats each AAdvantage card as a separate product.

So if you just picked up a Citi AAdvantage Platinum card, you can still apply for the Citi AAdvantage Executive card without waiting 48 months. All I’m saying is it could have been a lot worse.

Alternative: Barclay AAdvantage Aviator Red Card

If Citi’s new 48-month wait period between sign-up bonuses is dampening your card-churning plans, you can always pick up a Barclay AAdvantage Aviator Red Card instead. It currently has a better sign-up bonus than the Citi AAdvantage public offer: 60,000 miles after your first spend.

So even if you don’t qualify for a Citi card under the new 48-month waiting rule, you can still get an AAdvantage credit card but from a different bank.

Is Citi’s 48-month restriction on AAdvantage cards worse than 5/24?

My first thought when I saw the Citi 48-month restriction on AAdvantage card sign-up bonuses was, “Citi is about to pull a Chase 5/24.” But it’s not that bad. For starters, there are other AAdvantage sign-up bonuses you can get during that 48-month wait period—from Barclays and Citi, now that Citi treats all the cards as individual products.

Additionally, the Citi AAdvantage Platinum card is not in the same league as the affected Chase credit cards. I keep getting these cards and earning American miles because it’s so easy, but redeeming them can be a huge hassle.

Not to mention, I’ve now had two instances where I showed up at the airport with a confirmed ticket but couldn’t board my flight. American Airlines was super helpful, dropping my calls repeatedly and then sending me an email four days later asking me to call customer service to resolve the issue.

But enough of my complaining – I want to hear from you: Will Citi’s new 48-month restriction on AAdvantage card sign-up bonuses affect your churning strategy?

This may be off-topic but, given that you had the hammer brought down on you by Barclays a couple of years ago, do you think you’d be eligible for any of the Barclaycard bonuses?

Not off-topic at all. I probably won’t be eligible for the Barclay bonuses for a while.

Does this also apply to the CITI Business AA card?

Yes, the same rules apply to the business card. But if you got that card, you can still get one of the other Citi AA cards.

I feel your pain, Ariana, as Barclays shut me down two years ago. I tried to plead my case to their “Office of the President” department, but to no avail.

One of these days I’ll apply again for a Barclays card to see if the ban has been lifted, as I was told that it was not indefinite.

Let me know how that goes. It’s been over two years. I’d love to know at which point (if at all) Barclays will drop the grudge. 🙂

You can go around the rule if you are BUSINESS person and get the Citi AA Business card which gives you 75,000 miles and waives fee first year.

Yes. Every card is treated as a separate product.

My 24 month period since I closed Citi AA is coming in August -does it mean I have another 24 months to wait?

Yes. The new card language says 48 so you’ll have to wait another 24 before you’re eligible. You can, however, get the Business or Exec card. Barclays Aviator is another option.

Previously have to wait 24 months open and close the account. Is it now 48 months open? What about closing?

It’s within 48 months of getting your sign-up bonus. So if you pick up the card today and get your bonus in October, you’ll be eligible for another one in October 2023.

Does citi provide an easy way to know if you will be eligible for the bonus before applying?

Not that I know. You can check your account opening date in your credit report.

I prefer the new rule I was approved a few months ago for the Citi AA card only to realize I had closed my last card less than 24 months earlier. That silly part of the rule is finally gone. Now I can apply for other Citi AA cards while and earn miles.

Nice!

I just got this card back after 2 years. I think I would just sign up for the executive one next, then go back to Barclay. I’ve had excellent luck redeeming flights via Alaska.

I recently dumped Citi after their shenanigans (mailing my statement after the due date, delaying crediting my payment, etc in an effort to wrack up charges and boost interest rate). I like the idea of an AA card so I got the Barclays Aviator. Very happy with it so far.

That is so not ok. I’m actually good with Citi right now. They did a great job handling the fraud issues I wrote about a while ago. Wish I could say the same thing about American Express.

That sounds like a good strategy. Though TBH the Executive card sign-up bonus would have to be a lot higher (75k at least) for me to consider it.

Pingback: Citi Adds 48 Month Restriction on AAdvantage Credit Card Sign-up Bonuses - airwebtravel.net